Happy Diwali to all…

Happy Dhanteras..

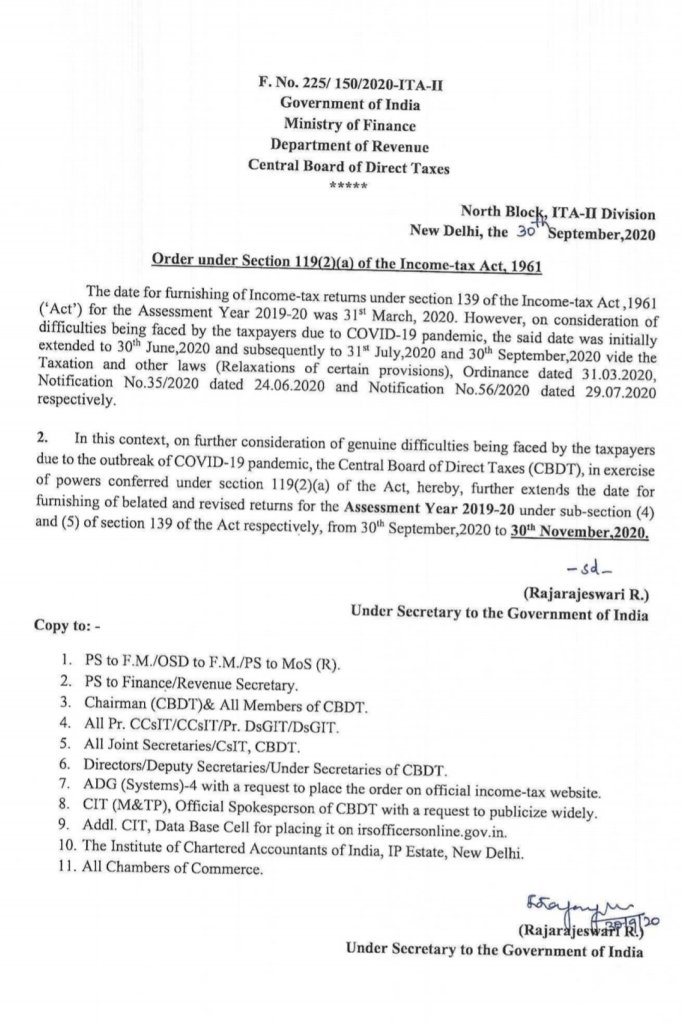

Income Tax Return – Due date Extended for FY 2018-19

The Ministry of Finance had extended the last date for filing belated returns and revised returns for Financial Year 2018-19 (Assessment Year 2019-20) to 30th November, 2020.

The Copy of the order is given below:

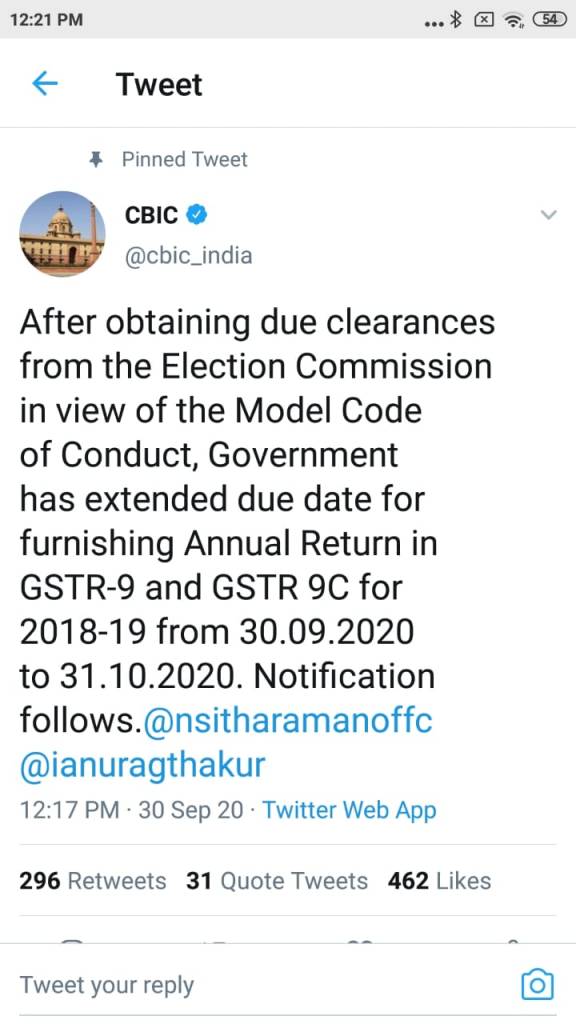

GST Annual Return – FY 2018-19 – Date extended

Central Board of Indirect Taxes and Customs (CBIC), in a recent tweet informed that the due date for filing Annual Returns of Financial Year 2018-19 in GSTR-9 and GSTR-9C is extended to 31.10.2020 from 30.09.2020. As per the tweet, notification will be issued later.

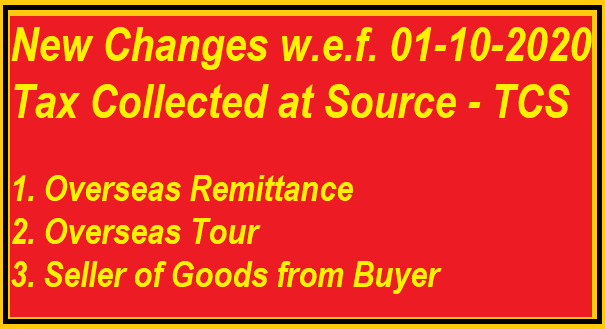

New Changes in Income Tax w.e.f. 01st October, 2020

The Changes that will take effect in the Tax Collected at Source provisions is discussed below:

| Sl No. | Particulars | Authorised Dealer | Overseas Tour Program | Seller of Goods |

| 1 | Who has to deduct? | An authorised dealer, who receives an amount, for remittance out of India from a buyer, | A seller of an overseas tour program package | A seller whose turonver during the financial year immediately preceding the financial year is more than ten crore Rupees, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year from a buyer. |

| 2 | From Whom to deduct? | A person remitting such amount out of India under the Liberalised Remittance Scheme of the Reserve Bank of India | A buyer, being the person who purchases such package | A buyer who purchase goods and pays consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year. |

| 3 | Any Exemption / Limit? | The amount or aggregate of the amounts being remitted by a buyer is less than seven lakh rupees in a financial year and is for a purpose other than purchase of overseas tour program package | Nil | Goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year. |

| 4 | When to Deduct? | At the time of debiting the amount payable by the buyer; or At the time of receipt of such amount from the said buyer, by any mode, whichever is earlier, | At the time of debiting the amount payable by the buyer; or At the time of receipt of such amount from the said buyer, by any mode, whichever is earlier, | At the time of receipt of such amount |

| 5 | Rate of TCS? | A sum equal to 5% on amount above seven lakh rupees in normal cases A sum equal to one half per cent of the amount or aggregate of the amounts in excess of seven lakh rupees remitted by the buyer in a financial year, if the amount being remitted out is a loan obtained from any financial institution as defined in section 80E, for the purpose of pursuing any education | A sum equal to five per cent of such amount as income-tax | A sum equal to 0.1 per cent of the sale consideration exceeding fifty lakh rupees as income-tax: |

| 6 | Instances where TCS not applicable? | (i) liable to deduct tax at source under any other provision of this Act and has deducted such amount; (ii) the Central Government, a State Government, an embassy, a High Commission, a legation, a commission, a consulate, the trade representation of a foreign State, a local authority as defined in the Explanation to clause (20) of section 10 or any other person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein. | (i) liable to deduct tax at source under any other provision of this Act and has deducted such amount; (ii) the Central Government, a State Government, an embassy, a High Commission, a legation, a commission, a consulate, the trade representation of a foreign State, a local authority as defined in the Explanation to clause (20) of section 10 or any other person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein. | (i) if the buyer is liable to deduct tax at source under any other provision of this Act on the goods purchased by him from the seller and has deducted such amount. (ii) (A) the Central Government, a State Government, an embassy, a High Commission, legation, commission, consulate and the trade representation of a foreign State; or (B) a local authority as defined in the Explanation to clause (20) of section 10; or (C) a person importing goods into India or any other person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein; |

Disclaimer: The posts made in this platform is for serving as an informative guide and is meant for general guidance and no responsibility for loss arising to any person acting or refraining from acting as a result of any material contained in posts made by us in this platform will be accepted by us. Users are requested to verify the validity of content before taking informed decisions.

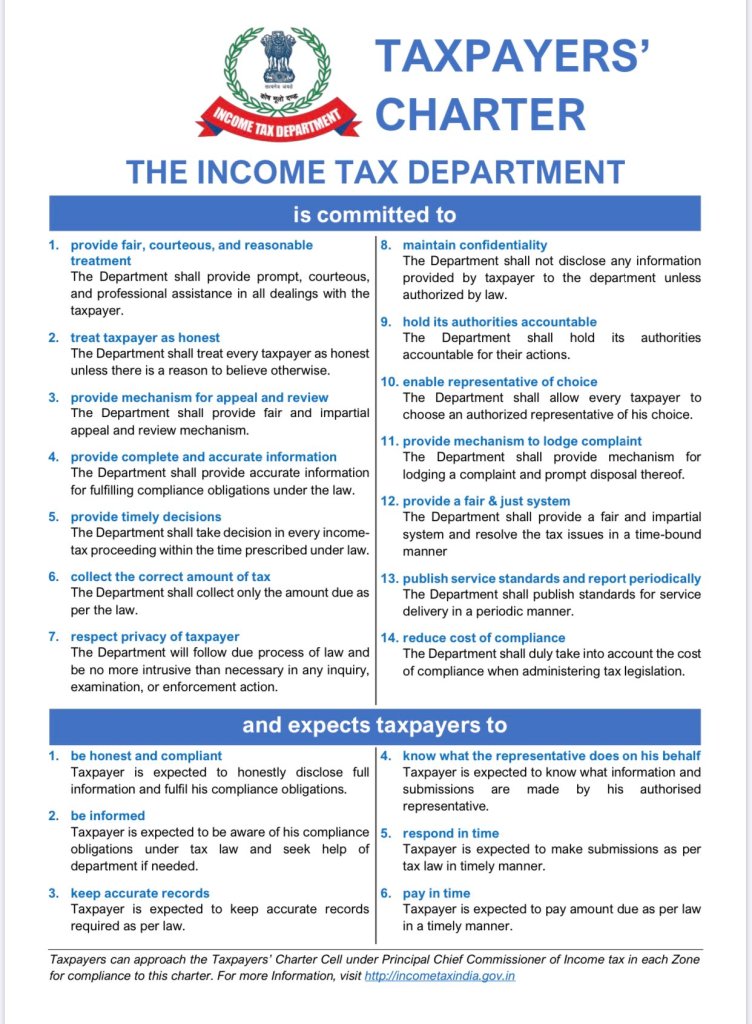

Tax Payers Charter

The Complete taxt is given below:

TAXPAYERS‘ CHARTER

THE INCOME TAX DEPARTMENT

is committed to

1. provide fair, courteous, and reasonable treatment

The Department shall provide prompt, courteous, and professional assistance in all dealings with the taxpayer.

2. treat taxpayer as honest

The Department shall treat every taxpayer as honest unless there is a reason to believe otherwise.

3. provide mechanism for appeal and review

The Department shall provide fair and impartial appeal and review mechanism.

4. provide complete and accurate information

The Department shall provide accurate information for fulfilling compliance obligations under the law.

5. provide timely decisions

The Department shall takedecision in every income tax pro ceedi ng within the time prescribed under law.

6. collect the correct amount of tax

The Department shall collect only the amount due as per the law.

7. respect privacy of taxpayer

The Department will follow due process of law and be no more intrusive than necessary in any inquiry, examination, or enforcement action.

8. maintain confidentiality

The Department shall not disclose any information provided by taxpayer to the department unless authorized by law.

9. hold its authorities accountable

The Department shall hold its authorities accountable for their actions.

10. enable representative of choice

The Department shall allow every taxpayer to choose an authorized representative of his choice.

11. provide mechanism to lodgecomplaint

The Department shall provide mechanism for lodging a complaint and prompt disposal thereof.

12. provide a fair & just system

The Department shall provide a fair and impartial system and resolve the tax issues in a time-bound manner

- publish service standards andreport periodically The Department shall publish standards for service delivery in a periodic manner.

14. reduce cost of compliance

The Department shall duly take into account the cost of compliance when administering tax legislation.

and expects taxpayers to

1. be honest and compliant

Taxpayer is expected to honestly disclose full information and fulfil his compliance obligations.

2. be informed

Taxpayer is expected to be aware of his compliance obligations under tax law and seek help of department if needed.

3. keep accurate records

Taxpayer is expected to keep accurate records required as per law.

4. know what the representative does on his behalf

Taxpayer is expected to know what information and submissions are made by his authorised representative.

5. respond in time

Taxpayer is expected to make submissions as per tax law in timely manner.

6. pay in time

Taxpayer is expected to pay amount due as per law in a timely manner.

Taxpayers can approach the Taxpayers‘ Charter Cell under Principal Chief Commissioner of Income tax in each Zone for compliance to this charter. For more Information, visit http://incometaxindia.gov.io

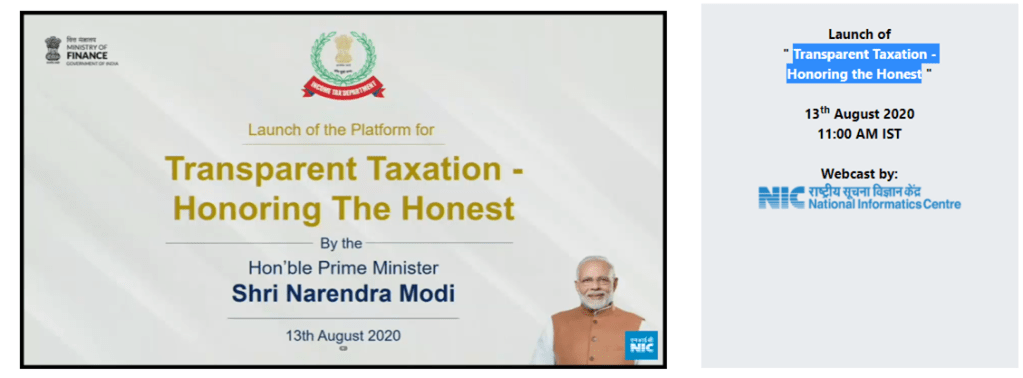

New Reforms in Taxation

Faceless assessment will start from today. Any assessment, other than exception, outside faceless assessment will be invalid.

Faceless appeal will also be launched on 25th September, 2020.

No intrusive and survey operations by field officers – Only investigation wing and TDS wing can after approval by the officer of the level of Commissioner or above.

Tax payers Charter introduced from today.

The platform being launched today brings in a transparent, efficient and accountable tax administration. It uses technology, Data Analytics and Artificial Intelligence – Finance Minister

Transparent Taxation – Honoring the Honest

Finance Minister, in her address the various reforms/steps taken by Income Tax Department like faceless assessement, simplification of forms, reduction in Corporate tax rate, Vivad Se Viswas Scheme etc.

FM virtually Launched the Platform Transparent Taxation – Honoring the Honest

Face less assessment and Tax Payers Charter is effective from today.

New arrangements, new facilities, starting today, strengthen our commitment to Minimum Government, Maximum Governance. This is a big step in the direction of reducing the interference of the government from the life of the countrymen

Atmanirbhar Bharath Abhiyan – FM Announcement Direct Taxes Proposal

TDS/TCS rates (except salary) will be reduced by 25% from tomorrow till 31st March, 2021. Eg. for Professionals the tax rate u/s.194J was 10%, which will be reduced to 7.50%.

All pending refunds shall be issued immediately.

Due date of all Income Tax Returns due date extended to 30th November, 2020.

Tax Audit due date extended to 31st October, 2020.

Assessment getting barred on 30-09-2020 is extended to 31-12-2020 and assessment getting time barred on 31-03-2021 is extended to 30-09-2021.

Vivad se viswas scheme is extended till 31-12-2020 without any additional fees