Mega Pension Scheme for Un-Organised Pension Scheme for organised sectors having income below Rs.15,000/-. till 60 years and Govt will contribute equal contribution. For a person of 29 years age, monthly contribution will be Rs.100/-. Rs.3000/- pension after 60 years.

Assured Income Support for Small and marginal farmers holding up-to 2 Hectares – New Scheme Launched – Rs.6000/- to farmers by Direct Account Transfer Scheme in 3 installments of Rs.2000 each. A wholly Central Govt Sponsored Scheme. Rs.75000 crore for FY 2019-20 and Rs.20000 crore in current year and the same will be implemented this year itself.

Rs.750 crores for Animal Husbandry and Fisheries for 2018-19

Fisheries – Seperate Department will be constituted. Benefit of 2% interest subvention for Animal Husbandry and fisheries.Additional 3% interest subvention for timely repayment.

All farmers affected by national calamity, who reschedule loan will get 2% interest subvention and 3% interest subvention for rescheduled period als0.

CBIC had

issued a Circular No.72/46/2018-GST dated 26th October, 2018, stating the

procedures to be followed when time expired drugs and medicines are returned

back to manufacturer through supply chain. In the circular, two

options/procedures are given. The same are:

Return

of the Time Expired Goods to be treated as fresh supply

Return

of time expired goods using credit note

The two options are discussed below:

Return of the Time Expired Goods to be treated as fresh supply

In case the goods returned is destroyed by the

manufacturer, the manufacturer is required to reverse the Input tax Credit (ITC

) availed on the return supply. ITC that need to be reversed in such scenario

is the ITC availed on return supply and not ITC that is attributable to

manufacture of such expired goods.

Illustration:

Supposedly, manufacturer has availed ITC of Rs. 10/- at the time of manufacture

of medicines valued at Rs. 100/-. At the time of return of such medicine on the

account of expiry, the ITC available to the manufacturer on the basis of fresh

invoice issued by wholesaler is Rs. 15/-. So, when the time expired goods are

destroyed by the manufacturer he would be required to reverse ITC of Rs. 15/-

and not of Rs. 10/-.

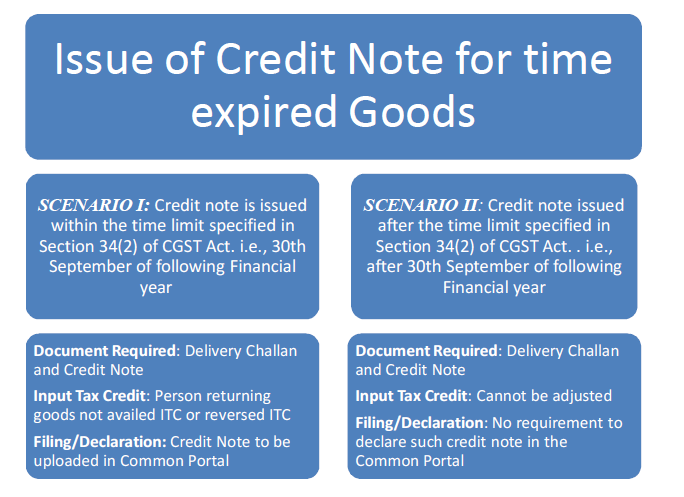

Return

of time expired goods by issuing credit note

As per sub-section (1) of Section 34 of the CGST Act the supplier can issue a credit note where the goods are returned back by the recipient. Thus, the manufacturer or the wholesaler who has supplied the goods to the wholesaler or retailer, as the case may be, has the option to issue a credit note in relation to the time expired goods returned by the wholesaler or retailer, as the case may be. As per law, there is no time limit for issuing of Credit Note. But, when it comes to adjustment of tax liability, the following scenarios may arise:

It is also clarified that, the circular will be applicable to other scenarios, where the goods are returned on account of reasons other than return of expired goods.

Disclaimer: Users are requested to verify the validity of content before taking informed decisions.