Pension benefits will be offered to 3 crore shopowners with annual turnover of less than Rs 1.5 crore under new scheme called Pradhan Mantri Man dhan Scheme, she says.

The government will examine options of opening up FDI in media, animation and some other sectors to improve these flows further, she says.

100% FDI in Insurance Intermediaries

Contemplating Conduction Global Investors Meet

Commercial arm, a public limited company incorporated to capitalise India’s Space Technology

CBIC vide circular no. 02/21/2019-GST dated 28th June, 2019 clarified taxability of penal interest on EMI payments. The circular discuss about two scenarios involving EMI transactions, and the same is reproduced below:

Case — 1:

X sells a mobile phone to Y. The cost of mobile phone is Rs 40,000/-. However, X gives Y an option to pay in installments, Rs 11,000/- every month before 10th day of the following month, over next four months (Rs 11,000/- *4 = Rs. 44,000/-). Further, as per the contract, if there is any delay in payment by Y beyond the scheduled date, Y would be liable to pay additional / penal interest amounting to Rs.500/- per month for the delay. In some instances, X is charging Y Rs. 40,000/- for the mobile and is separately issuing another invoice for providing the services of extending loans to Y, the consideration for which is the interest of 2.5% per month and an additional / penal interest amounting to Rs. 500/- per month for each delay in payment.

Analysis:

As per the provisions of sub-clause (d) of sub-section (2) of section 15 of the CGST Act, the value of supply shall include “interest or late fee or penalty for delayed payment of any consideration for any supply”.

As per the provisions of sub-clause (d) of sub-section (2) of section 15 of the CGST Act, the amount of penal interest is to be included in the value of supply. The transaction between X and Y is for supply of taxable goods i.e. mobile phone. Accordingly, the penal interest would be taxable as it would be included in the value of the mobile, irrespective of the manner of invoicing.

Case — 2:

X sells a mobile phone to Y. The cost of mobile phone is Rs 40,000/-. Y has the option to avail a loan at interest of 2.5% per month for purchasing the mobile from M/s ABC Ltd. The terms of the loan from M/s ABC Ltd. allows Y a period of four months to repay the loan and an additional / penal interest @ 1.25% per month for any delay in payment.

Analysis

In terms of Sl. №27 of notification №12/2017- Central Tax (Rate) dated the 28.06.2017 “services by way of (a) extending deposits, loans or advances in so far as the consideration is represented by way of interest or discount (other than interest involved in credit card services)”is exempted. Further, as per clause 2 (zk) of the notification №12/2017-Central Tax (Rate) dated the 28th June, 2017, “‘interest’ means interest payable in any manner in respect of any moneys borrowed or debt incurred (including a deposit, claim or other similar right or obligation) but does not include any service fee or other charge in respect of the moneys borrowed or debt incurred or in respect of any credit facility which has not been utilised;”.

The additional / penal interest is charged for a transaction between Y and M/s ABC Ltd., and the same is getting covered under Sl. №27 of notification №12/2017- Central Tax (Rate) dated 28.06.2017. Accordingly, in this case the ‘penal interest’ charged thereon on a transaction between Y and M/s ABC Ltd. would not be subject to GST, as the same would not be covered under notification №12/2017-Central Tax (Rate) dated 28.06.2017. The value of supply of mobile by X to Y would be Rs. 40,000/- for the purpose of levy of GST.

It is further clarified that the transaction of levy of additional / penal interest does not fall within the ambit of entry 5(e) of Schedule II of the CGST Act i.e. “agreeing to the obligation to refrain from an act, or to tolerate an act or a situation, or to do an act”, as this levy of additional / penal interest satisfies the definition of “interest” as contained in notification №12/2017- Central Tax (Rate) dated 28.06.2017.

It is further clarified that any service fee/charge or any other charges that are levied by M/s ABC Ltd. in respect of the transaction related to extending deposits, loans or advances does not qualify to be interest as defined in notification №12/2017- Central Tax (Rate) dated 28.06.2017, and accordingly will not be exempt.

GST Council in its 35th meeting recommended following schedule for implementation of new GST returns. The recommendations are given below:

A. For Small tax payers (those having turnover of upto Rs. 5 Crores in previous financial year)

i) Form GST ANX-1: Quartely starting from period October, 2019 to December, 2019 in January, 2020.

ii) Form GST RET-01: Quartely starting from period October, 2019 to December, 2019 in January, 2020.

iii) Form GST PMT-08: To filed from October, 2019

Note: Form GSTR-3B need not be filed from October,2019

B. Large Tax Payer (those having turnover of more than Rs. 5 Crores in previous financial year)

i. Form GST ANX-1: Compulsory filing from October 2019

ii. Form GSTR-3B: To be filed for October 2019 & November 2019

iii. Form GST RET-01: To be filed from December 2019

It is also decided that Form GST ANX-I and Form GST ANX-2 will be available on trial basis to taxpayers between July 2019 to September 2019.

There will be an option to upload Invoices etc. FORM GST ANX-1 on a continuous basis both by large and small taxpayers from October 2019 onwards. During this period, FORM GST ANX-2 may be viewed simultaneously, but no action can be taken.

GSTR-3B will be completely phased out by January, 2020.

Government of India had reduced the contribution under ESI Act, to 4% from the existing 6.50% as per the press release issued by Ministry of Labour and Employment dated 13th June, 2019. The Contribution by employers is reduced to 3.25% from the existing 4.50% and the contribution of employees is reduced to 0.75% from the existing 1.75. The reduction in rates would benefit 3.60 crores of employees and 12.85 lakhs employers as per the press release. The reduction will be applicable from 01st July 2019 as per the press release. The entire text of the press release is given below:

The Government of India has taken a historic decision to reduce the rate ofcontribution under the ESI Act from 6.5% to 4%(employers’ contribution beingreduced from 4.75% to 3.25% and employees’ contribution beingreducedfrom 1.75% to 0.75%). Reduced rates will be effective from 01.07.2019.Thiswould benefit 3.6 crore employees and 12.85 lakhemployers.

The reduced rate of contribution will bring about a substantial relief to workers and it will facilitate further enrollment of workers under the ESI scheme and bring more and more workforce into the formal sector. Similarly, reduction in the share of contribution of employers will reduce the financial liability of the establishments leading to improved viability of these establishments. This shall also lead to enhanced Ease of Doing Business. It is also expected that reduction in rate of ESI contribution shall lead to improved compliance oflaw.

The Employees’ State Insurance Act 1948 (the ESI Act) provides for medical, cash, maternity, disability and dependent benefits to the Insured Persons under the Act. The ESI Act is administered by Employees’ State Insurance Corporation (ESIC). Benefits provided under the ESI Act are funded by the contributions made by the employers and the employees.

Under the ESI Act, employers and employees both contribute their shares respectively. The Government of India through Ministry of Labour and Employment decides the rate of contribution under the ESI Act. Presently, the rate of contribution is fixed at 6.5% of the wages with employers’ share being 4.75% and employees’ share being 1.75%. This rate is in vogue since01.01.1997.

The Government of India in its pursuit of expanding the Social Security Coverage to more and more people started a programme of special registration of employers and employees from December, 2016 to June, 2017 and also decided to extend the coverage of the scheme to all the districts in the country in a phased manner. The wage ceiling of coverage was also enhanced from Rs. 15,000/- per month to Rs. 21,000/- from01.01.2017.

These efforts resulted insubstantial increase in the number of registeredemployees i.e. Insured Persons and employersand also a quantum jump in therevenue income of the ESIC.The figures are as under: –

Year

No. of Employers

No. of Insured Persons (in crores)

Total contribution received(in Rs. crores)

2015-16

7,83,786

2.1

11,455

2016-17

8,98,138

3.1

13,662

2017-18

10,33,730

3.4

20,077

2018-19

12,85,392

3.6

22,279

The Government of India is committed to the cause of welfare of employees as well asemployers.

It is also committed to improve the quality of medical services & other benefits being provided under the ESI scheme.

rcj/skp-ESI rate reduction13-04-2019 (Release ID :190452)

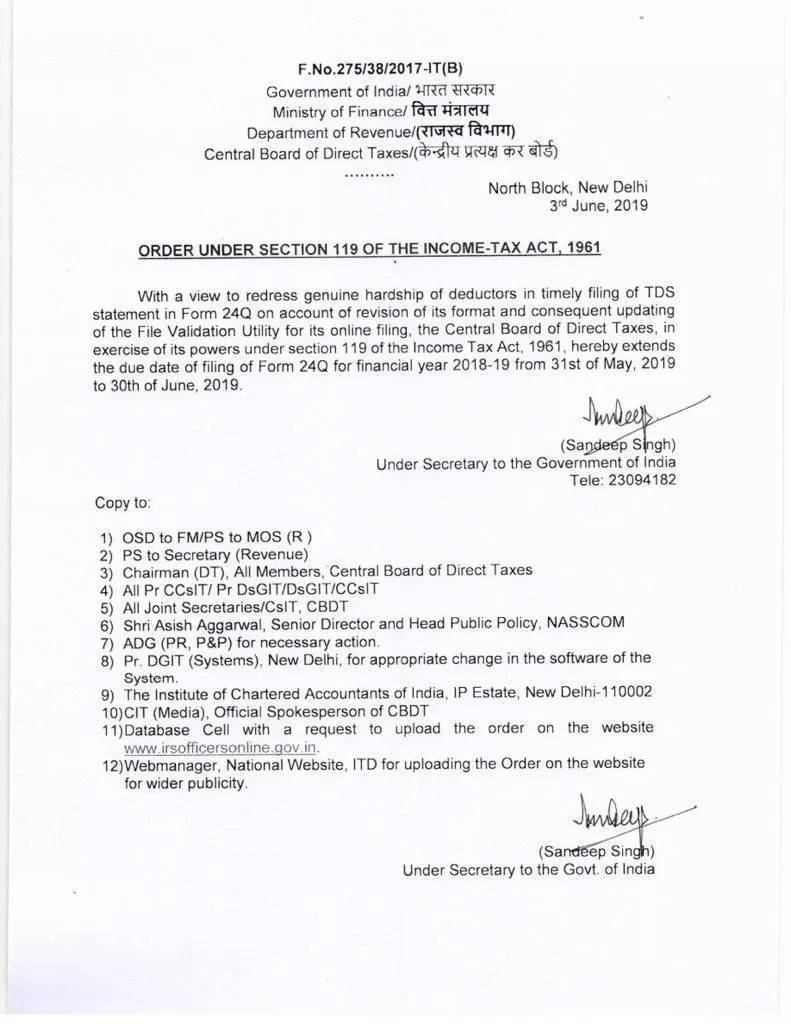

Central Board of Direct Taxes, had issued an order u/s. 119 of Income Tax Act, 1961 (F NO.275/38/2017-IT(B)) dated 03rd June, 2019), extending the due date of furnishing Tax Deducted at Source return of Salary (Form 24Q) for the last quarter of the financial year 2018-19 from 31st May, 2019 to 30th June, 2019.

The order states that this has been done in order to redress the genuine hardships of deductors in timely filing of TDS statement in Form 24Q, on account of revision of its format and consequent updating of the File Validation Utility for its online filing. The copy of the order is given below:

The extension of due date may also lead to extension of due date of filing Income Tax Returns for Individuals and other assessees who are not covered by audit under Income Tax Act or any other statute. The due date for filing Income Tax returns is 31st July, 2019. The Form 16 (TDS Certificate) will be issued by employers by 10th July, 2019 only and the assessee will be getting only 21 days to file the Income Tax Return if the due date of 31st July is not changed.