DPDP Series 2, Episode 1.1

Priya’s Story

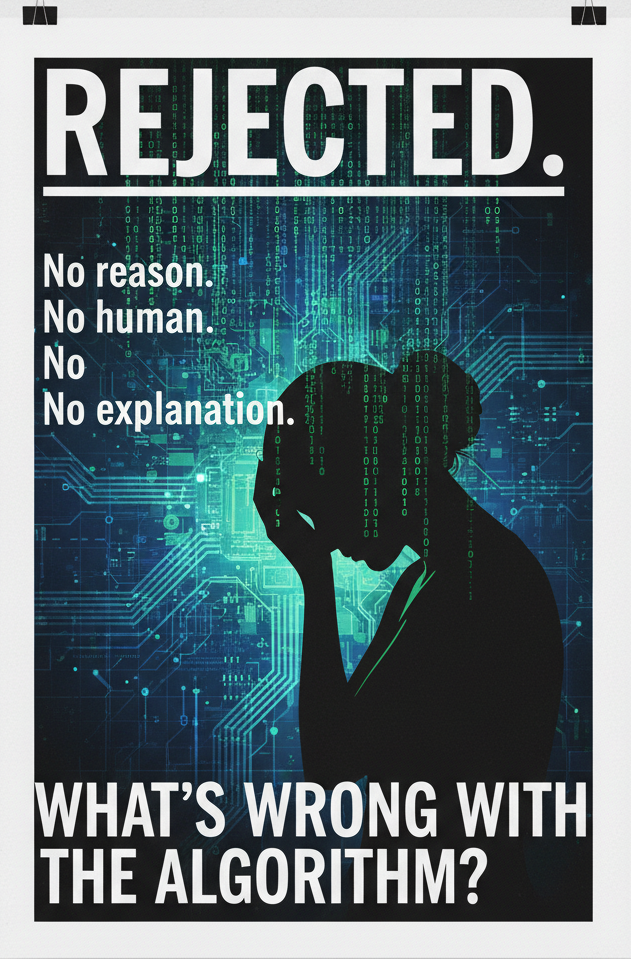

The AI That Rejected Her Home Loan Without Reading Her File

Priya is a 31-year-old schoolteacher in a village in Tirunelveli. Clean credit history. Stable government salary. Zero defaults.

She applies for a home loan through a fintech platform. Within seconds, the response arrives: Rejected.

No reason. No human. No explanation. An AI credit-scoring algorithm made the call — silently, instantly, and without looking her in the eye.

She tries a second platform. Same outcome. She begins to wonder what is wrong with her, when the real question is: what is wrong with the algorithm?

Why AI credit scoring creates a DPDP problem

IS Audit Module 6 of the ICAI IS Audit 3.0 Course is direct: AI is widely used in banking apps to provide a faster, more accurate assessment of a potential borrower at less cost, accounting for a wider variety of factors. Credit scoring provided by AI is based on more complex and sophisticated rules compared to traditional systems.

More complex. More factors. And entirely invisible to Priya.

The problem is this: Priya’s loan application was rejected because the AI model had never meaningfully encountered a borrower profile like hers — a government employee in a Tier-3 city, with a savings-heavy profile and no credit card history — trained predominantly on urban, credit-card-using, high-transaction-volume data. IS Audit Module 6 names this explicitly: datasets applicable to AI applications to learn are really rare. Models trained on incomplete data produce biased outcomes for underrepresented groups.

The algorithm was not wrong about what it was trained to do. It was wrong about what it was trained on. And Priya paid the price.

The DPDP dimension — consent was not built for this

When Priya downloaded the fintech app and applied for the loan, she tapped “I Agree” to a terms-of-service document she likely did not read in full. That consent, under the DPDP Act, 2023, is not valid for everything the AI subsequently did with her data.

Section 6(1) of the DPDP Act is unambiguous: consent must be free, specific, informed, unconditional and unambiguous, limited to such personal data as is necessary for the specified purpose.

The specified purpose was loan evaluation. But the AI ingested Priya’s location history, app usage patterns, device behaviour, social interactions, and transaction metadata — far beyond what is necessary to evaluate creditworthiness. Every data element beyond the specified purpose is processing without a valid basis.

Furthermore, if her data was used to train or refine the AI model — improving the algorithm for future use — that is a separate processing purpose that required separate consent. She did not give it. Section 6(1) requires each distinct purpose to be separately consented to.

The right she did not know she had

Under Section 11 of the DPDP Act, Priya has the right to access a summary of all personal data being processed about her — including the processing activities undertaken. She has the right to ask what the algorithm used, what it concluded, and why.

Under Section 13, she has the right to raise a grievance with the Data Fiduciary. An AI system that cannot explain its decision — cannot identify what data points drove the rejection — cannot satisfy this right. A black-box model is, under DPDP, a grievance waiting to happen.

The CERT-In Guidelines on Secure Adoption and Governance of Artificial Intelligence Systems (Version 1.0, 25 May 2026) identify Human Oversight and Decision Governance as a mandatory control: validate AI-generated outputs, restrict fully autonomous critical actions, and maintain auditability and approval mechanisms. An AI that rejects a loan application with no human review and no audit trail fails every limb of this control.

The question every AI-first fintech must answer

Can you tell Priya — specifically, in relation to her file — what personal data the algorithm used, whether that data was within the scope of her consent, and how it contributed to the rejection decision?

If the answer is “our model doesn’t work that way” — the compliance gap is not in the algorithm. It is in the governance architecture around it.

The DPDP Act is not asking AI to stop working. It is asking AI to work accountably.

Disclaimer

The contents of this post are intended for general awareness and informational purposes only. They do not constitute legal opinion, professional advice, consultancy, statutory interpretation, or a recommendation to act in any particular manner.

The Digital Personal Data Protection Act, 2023, related rules, notifications, regulatory guidance and judicial interpretations may evolve from time to time. The applicability of the law may also vary depending on the facts, sector, nature of data processing, organisational role, contractual terms and compliance framework.

Readers should not rely solely on this post for making legal, business, HR, technology, data-processing or compliance decisions. Specific advice from a qualified legal, privacy, cybersecurity, governance or compliance professional should be obtained before acting on any matter discussed.

The author / publisher shall not be responsible for any loss, liability, claim, penalty or consequence arising from reliance on the contents of this post without independent professional advice.

Authors:

This article has been co-authored by CA. Sunil Elayadath and CA. Karthik Narayanan S, Partners of Karthik & Sunil, together with Mr. Dhanesh P. K., Designated Partner, DSK Sustainability Tech.